Most people know that if you sell something for more than you paid for it, HMRC may want a slice of the profit.

What many people are less clear on is how this works with houses.

The short version is this: you do not normally pay Capital Gains Tax when you sell your own main home, provided it has genuinely been your only or main residence throughout the time you owned it.

That is because of Private Residence Relief.

But the position changes if the property has not always been your main home. For example, if you moved out and kept it as a rental property, or if you bought a second property as an investment, you may well have a Capital Gains Tax bill when it is sold.

To clarify how this works in practice, let’s look at a few simple examples.

As always, this is general guidance only. Capital Gains Tax can get fiddly very quickly, so you should speak to your accountant or tax adviser before selling.

Example 1: Selling your main home

Let’s start with the easy one.

Sarah bought her home in 2016 for £180,000.

She lived in it as her only home the whole time.

In 2026, she sells it for £260,000.

On paper, Sarah has made a gain of £80,000.

But because the property was her main residence throughout the whole period of ownership, she should normally get full Private Residence Relief.

That means:

| Item | Amount |

| Purchase price | £180,000 |

| Sale price | £260,000 |

| Paper gain | £80,000 |

| Private Residence Relief | £80,000 |

| Taxable gain | £0 |

| Capital Gains Tax | £0 |

So, although Sarah has “made” £80,000, she does not pay Capital Gains Tax on that gain.

This is the typical outcome when you sell a home you truly lived in.

Example 2: Lived in the house, moved out, rented it, then sold it later

This is where people often get caught.

Let’s say Michael bought a house in 2014 for £160,000.

His purchase costs, including legal fees, survey and stamp duty, came to £3,000.

He lived in the property as his main home for 5 years.

He then moved out, kept the property, and rented it for the next 7 years.

In 2026, he sells the house for £300,000.

His estate agent, legal and selling costs come to £6,000.

A valuation was taken when he moved out, showing the property was worth approximately £220,000 at that time. That valuation may be useful background evidence, but the Private Residence Relief calculation is usually based on the period of ownership, not simply the value on the day he moved out.

Here is the calculation.

| Item | Amount |

| Sale price | £300,000 |

| Less selling costs | £6,000 |

| Net sale proceeds | £294,000 |

| Purchase price | £160,000 |

| Purchase costs | £3,000 |

| Total base cost | £163,000 |

| Total gain | £131,000 |

Michael owned the property for 12 years, or 144 months.

He lived in it for 5 years, or 60 months.

Because it was once his main home, he also gets relief for the final 9 months of ownership.

So his qualifying period is:

60 months + 9 months = 69 months

So 69 out of 144 months qualify for Private Residence Relief.

| Calculation | Amount |

| Total gain | £131,000 |

| Private Residence Relief: 69 / 144 | £62,770 approximately |

| Remaining chargeable gain | £68,230 approximately |

| Less annual CGT allowance | £3,000 |

| Taxable gain | £65,230 approximately |

If Michael is a higher-rate taxpayer, and assuming the gain falls into the 24% residential property CGT rate, the tax would be roughly:

£65,230 × 24% = £15,655

Despite having lived there, Michael faces a Capital Gains Tax bill of around £15,655.

The point is simple: moving out and keeping your old home can create a future tax bill.

Not the entire gain is taxable, nor is it fully protected.

Example 3: Buying a rental property and building an extension

Now let’s look at a pure investment property.

Emma buys a rental property in 2018 for £120,000.

Her purchase costs, including legal fees and stamp duty, are £4,000.

A few years later, she builds an extension costing £45,000.

This is important. A genuine improvement, such as an extension, can normally be deducted when working out the gain. Ordinary repairs and maintenance cannot usually be deducted in the same way for Capital Gains Tax purposes.

In 2026, Emma sells the property for £245,000.

Her selling costs are £5,000.

Here is the calculation.

| Item | Amount |

| Sale price | £245,000 |

| Less selling costs | £5,000 |

| Net sale proceeds | £240,000 |

| Purchase price | £120,000 |

| Purchase costs | £4,000 |

| Extension cost | £45,000 |

| Total allowable cost | £169,000 |

| Gain | £71,000 |

| Less annual CGT allowance | £3,000 |

| Taxable gain | £68,000 |

If Emma is a higher-rate taxpayer, and the residential property CGT rate is 24%, the tax would be:

£68,000 × 24% = £16,320

So Emma sells the property for £125,000 more than she paid for it, but once purchase costs, sale costs and the extension are deducted, her taxable gain is much lower.

Even after deductions, Emma’s tax bill exceeds £16,000.

That is not exactly pocket change.

What costs can you usually deduct?

When calculating the gain, you can usually deduct costs such as legal fees, stamp duty, and agent’s commissions that are associated with buying, selling, or improving the property.

These may include:

- legal fees on purchase and sale;

- estate agent’s fees;

- stamp duty;

- survey or valuation fees;

- improvement works, such as an extension.

But you cannot simply deduct all expenses related to the property. Only certain specific expenses are allowed as deductions under established rules.

Normal repairs, redecorating, replacement carpets, routine maintenance, and mortgage interest are not typically deductible when working out Capital Gains Tax. These are considered ongoing or routine costs, not qualifying improvements.

Keep proper records. Keep invoices. Keep valuations. Keep completion statements.

Your future self will thank you.

Joint owners

If a property is jointly owned, each owner may have their own annual CGT allowance and their own tax position.

That can make a significant difference.

For example, if a husband and wife jointly own a rental property, the gain may be split between them. Each may be able to use their own annual exemption, and each person’s income tax position may affect the CGT rate payable.

Again, this is one for proper tax advice before the sale completes, not after.

The 60-day reporting trap

If you sell a UK residential property and there is Capital Gains Tax to pay, you usually need to report and pay the tax within 60 days of completion.

This catches people out.

It is not something to leave until the next tax return, dusted off months later with a cup of tea and a rising sense of panic.

If you think there may be Capital Gains Tax to pay, speak to your accountant before completion.

The slightly annoying inflation point

There is one final point which is worth making.

House prices are usually talked about in pounds.

You bought it for £100,000.

You sold for £180,000.

Lovely. You made £80,000.

You sold for £180,000.

Lovely. You made £80,000.

Except money itself changes value.

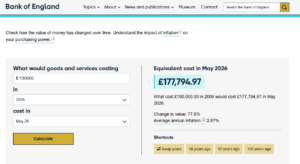

According to inflation calculations based on UK price data, £100,000 in 2006 is equivalent to £177,794 in 2026 money.

So if you bought a house for £100,000 in 2006 and sold it for £177,794 in 2026, it might look like you made nearly £80,000.

But in purchasing power terms, you may not really have gained anything at all.

In fact, you may be behind.

The tax system does not usually care about that. It looks at the nominal gain.

That means you can end up paying Capital Gains Tax on a gain which, in real-world spending power, may feel much less impressive than it looks on paper.

Fun, isn’t it?

Final thoughts

Capital Gains Tax on houses is not always complicated, but it is very easy to get wrong.

The broad rules are:

If it has always been your main home, you usually do not pay CGT.

If it was once your home but later became a rental property, part of the gain may be taxable.

If it was always a rental or investment property, the gain will usually be taxable, subject to allowable costs and reliefs.

If you are thinking of selling a second property, a former home, or a rental property, get the figures checked before you sell.

A bit of planning before completion is far better than a nasty letter from HMRC afterwards.

For official guidance, see the HMRC Capital Gains Tax guidance on GOV.UK.

If you need advice on capital gains tax property implications during a sale, please contact J.J. Taylor & Co Solicitors. We act for clients across Armagh, County Down and County Tyrone.