Inheritance Tax (IHT) planning has always been vital to protecting your estate and ensuring your Will reflects your current wishes. With the government announcing significant changes to Business Relief (BR) and Agricultural Relief (AR) effective from 6 April 2026, it is more important than ever to act now to safeguard your assets. We’ve already covered AR in detail, so today we’re covering Business Relief which will be changing in similar ways.

Inheritance Tax (IHT) planning has always been vital to protecting your estate and ensuring your Will reflects your current wishes. With the government announcing significant changes to Business Relief (BR) and Agricultural Relief (AR) effective from 6 April 2026, it is more important than ever to act now to safeguard your assets. We’ve already covered AR in detail, so today we’re covering Business Relief which will be changing in similar ways.

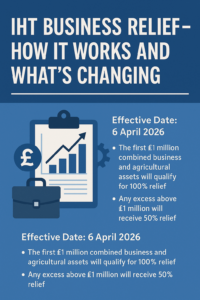

1. Overview of Upcoming Changes

- Effective Date: 6 April 2026

- Anti-Forestalling Period: From 30 October 2024 to 5 April 2026, any gifts or transfers you make may still be caught by the new rules if you pass away within seven years of the gift.

- Relief Cap:

- The first £1 million combined business and agricultural assets will qualify for 100% relief.

- Any excess above £1 million will receive 50% relief, equivalent to a 20% effective IHT rate on the excess.

Key Takeaway: These reforms mean significantly higher potential IHT liabilities for estates that exceed £1 million in qualifying business and agricultural assets.

2. What is Business Relief?

Business Relief (BR) is currently a powerful tool for business owners. It allows certain assets and trading businesses to pass on with either 50% or 100% relief from IHT, provided the qualifying conditions are met. This can help safeguard the continuity of a family business.

Qualifying Conditions

- Relevant Business Property (RBP) must be owned for at least two years before transfer.

- The business must be carried on to make a profit.

- The business cannot wholly or mainly deal in shares, land, or investments.

- No binding contract for sale should be in place.

- Excepted Assets (e.g., assets held mainly for personal use, sizeable unneeded cash balances) do not qualify for BR and remain chargeable to IHT.

Note: Transfers between spouses or civil partners may benefit from special rules, including crediting the ownership period of the first spouse to the survivor.

3. Reform Details from April 2026

- £1 Million at 100% Relief

- Beyond £1 million, BR/AR drops from 100% to 50%. The remaining taxable portion is effectively subject to 20% IHT (half the usual 40% rate).

- AIM-Listed Shares

- Currently treated as unquoted for 100% relief, but from 6 April 2026, they will qualify for only 50% relief, regardless of value.

- Unused allowance does not transfer to a surviving spouse.

- Anti-Forestalling Provisions

- Gifts made after 30 October 2024 will be assessed under the new regime if the donor dies within seven years of making the gift.

- Gifts before that date still qualify under the current rules if you survive for seven years.

- Instalment Payment & Interest-Free

- IHT on business property can still be paid in 10 annual instalments, interest-free, offering some mitigation of the tax burden.

4. Recommended Action for Business Owners

- Review Your Business Structure

- Confirm that your business or shares qualify for BR under current rules. Consider whether steps can bolster BR eligibility (e.g., reducing non-trading or “excepted assets”).

- Check Your Wills and Estate Plans

- Ensure each spouse potentially holds at least £1 million in BR-qualifying assets because unused allowances won’t transfer to a surviving spouse under the new rules.

- Consider Trusts Carefully

- While trusts remain a valuable estate-planning tool, new rules about multiple trusts and anti-forestalling provisions add complexity. Early action may lock in current relief levels.

- Stay Informed About Pensions

- The 2024 Autumn Budget proposes ending the IHT exemption for certain pensions from April 2027, which may also impact your estate plan.

- Consider Advance Clearance

- In some cases, you can apply to HMRC for an advance opinion on BR if you are about to make a chargeable transfer (e.g., a transfer to a trust). At the same time, you may claim holdover relief for Capital Gains Tax on the transfer.

5. Conclusion

The upcoming changes to IHT Business Relief and Agricultural Relief are substantial. Any business owner with assets likely to exceed £1 million in value should begin planning early—well before April 2026—to minimise future inheritance tax exposure and protect long-term family wealth.

If you have any questions about how these new rules might affect you or need tailored advice on estate planning and business succession, our team at JJ Taylor Solicitors is here to help. Contact us to discuss your options and ensure your legacy is protected.